Open Capital Market on Crypto Rails

At Blockwall, we are staunch advocates of the token economy, as it has been the main driver of our very first investment vehicle thesis (BWC I), raised back in 2017. At that time, the world was still grappling with the potential real-world applications of blockchain technology. Undeterred, we have consistently pursued innovations aimed at decentralizing financial markets and creating synergies between them.

While blockchain technology is gradually transforming segments of this industry, key aspects of traditional finance have yet to fully capitalize on these technological advancements.

Traditional finance, or "TradFi" as it's known in the crypto sphere, has long been a siloed domain, dominated by centralized entities like clearinghouses, depositories, trading venues, and banks. This centralized architecture has often stifled innovation by adding layers of cost through intermediaries, slowing down transactions, and obscuring market transparency.

The Rise of Real-World Assets (RWAs) Tokenization

RWA tokenization involves converting tangible and intangible assets into digital tokens, which are then securely stored, managed, and traded on a blockchain. This shift aims to replace traditional paper-based systems of asset ownership — like those for real estate, fine art, or equities — with blockchain technology. The result is streamlined trading, easier management, and fractional ownership, opening new pathways for asset liquidity and capital efficiency.

Among blockchain-driven innovations, the tokenization of real-world assets (RWAs) has long emerged as a clear evolutionary step in crypto, initially gaining strong momentun in the real estate and arts markets while opening up broader perspectives for securities.

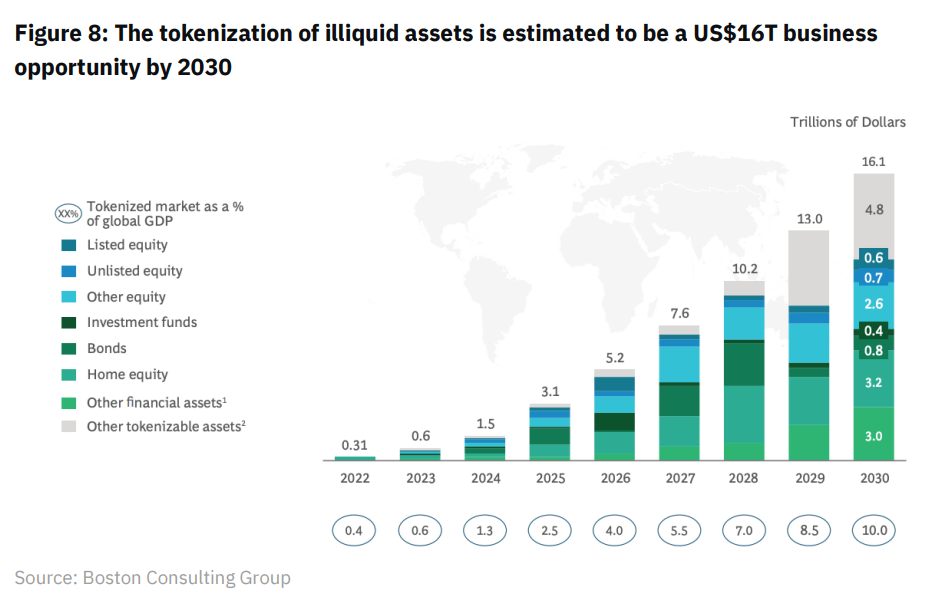

However, the RWA tokenization sector is still a burgeoning one but growing at an incredible pace. According to a report from BCG, the tokenized asset market is estimated to reach $16 trillion by 2030, a significant increase from $310 billion as of 2022. This would make up 10% of global GDP by the decade's end.

Even at US$16T, tokenized assets will still be a small fraction of the current total global asset value, estimated to be worth US$900T (less than 1.8%, to be exact, and not factoring in future global asset value growth). One may even argue that the true addressable market is the entire global asset market, given that anything tokenizable could be represented as RWAs on-chain.

These metrics highlight, on one hand, the rising demand for novel financial solutions within the blockchain arena to efficiently manage stablecoin liquidity, and on the other hand, how traditional financial assets have much to gain from blockchain efficiencies and security measures.

How do we make it happen ?

That's where Spiko comes in. They have a straightforward yet impactful mission: to serve as the connective tissue between traditional finance and DeFi. Their current focus is on bringing cash securities and instruments, such as cash management and risk-minimizing counterparty securities, available on-chain. Spiko plans to expand its market scope to include a broad array of assets, such as corporate bonds and stocks. In doing so, Spiko aims to augment the utility of stablecoins by offering an efficient alternative for the cash component of securities transactions.

Expanding on this, their long-term vision suggests that the integration of blockchain technology is redefining how securities are managed and traded. Securities should be directly issued and registered on interoperable public chains, opening up a range of custody options, including self-custody. This shift will transform traditional securities depositories into service providers specialising in custody and administration while transactions would benefit from atomic settlement, achieving near-instant finality and eliminating the need for clearing houses, except for managing marginal residual credit risk.

Spiko's initial product offering lays the groundwork for realizing their ambitious vision. They are developing Euro and US Dollar-based UCITS Money Market Funds (MMFs) and short-duration bond funds. All these instruments will be tokenized, enabling investors to seamlessly enter or exit based on their investment needs.

While some competition already exists in this space, Spiko intends to carve out its own niche, especially in the European Union where the Markets in Crypto-Assets (MICA) regulation is gradually taking effect. Spiko's competitive edge will stem from its robust regulatory infrastructure, harmonized with emerging market standards.

In light of recent regulatory developments in both the US and the EU, we at Blockwall firmly believe that regulatory alignment will act as a catalyst for the widespread adoption of on-chain securities and will encourage liquidity inflows into the web3 ecosystem.

However, the road to becoming the next "unicorn" in RWA tokenization is fraught with complexities. Success in this domain requires more than just technical prowess in decentralized finance (DeFi) and blockchain development. It necessitates a nuanced understanding of market dynamics, regulatory landscapes, and the intricacies of asset tokenization. This is a multidisciplinary challenge that calls for expertise in both traditional finance and emerging blockchain technologies.

Spiko's leadership is a testament to this philosophy, which is why we're humbled to actively back Paul-Adrien & Antoine as they both gather previous work experience as investors and policymakers.

Onward! 🚀

Learn more about Spiko:

Disclaimer

To avoid any misinterpretation, nothing in this blog should be considered as an offer to sell or a solicitation of interest to purchase any securities advised by Blockwall, its affiliates or its representatives. Under no circumstances should anything herein be interpreted as fund marketing materials for prospective investors considering an investment in any Blockwall fund. None of the data and information constitutes general or personalized investment advice and only represents the personal opinion of the author. The author and/or Blockwall may directly or indirectly be exposed to the mentioned assets/investments. For further information please view the full Disclaimer by clicking the button below.

This work is licensed under the Creative Commons Attribution – No Derivatives 4.0 International License. CC BY-ND 4.0 Legal Code | Creative Commons