An overview of (Re)Staking pt2

Building on Liquid Staking’s Foundations

In our last staking article, we’ve explored the rise of staking and PoS networks. By depositing tokens as collateral to validate transactions, stakers earn rewards while helping secure the chain. Yet as staking matured, crucial questions popped up: could staked tokens do even more than just earn rewards and secure a single network? The answer came in the form of liquid staking—token holders could stake their assets while receiving a derivative token (LSTs) to use in lending, borrowing, or trading. This step unleashed new capital efficiencies, making it possible for people to stay staked yet still participate in the broader decentralized finance (DeFi) ecosystem and allowing liquidity to flow.

From there, a newer paradigm took shape. If liquid staking derivatives allowed tokens to move freely while still being locked for consensus, why couldn’t these same tokens—already securing a main chain—be “restaked” to protect or bootstrap other protocols? This novel concept, known as restaking, has been riding a wave of interest as it offers stakers the potential to earn additional yields while expanding security for up-and-coming projects.

How EigenLayer Sparked a Restaking Revolution

Restaking’s rise isn’t just a lucky accident. It came about through the concerted efforts of research-oriented teams looking to reuse the staked collateral from major chains for new purposes. One of the most prominent catalysts was a platform that many credit with setting the restaking movement into motion: EigenLayer.

Thanks for reading Blockwall Insights! Subscribe for free to receive new posts and support my work.

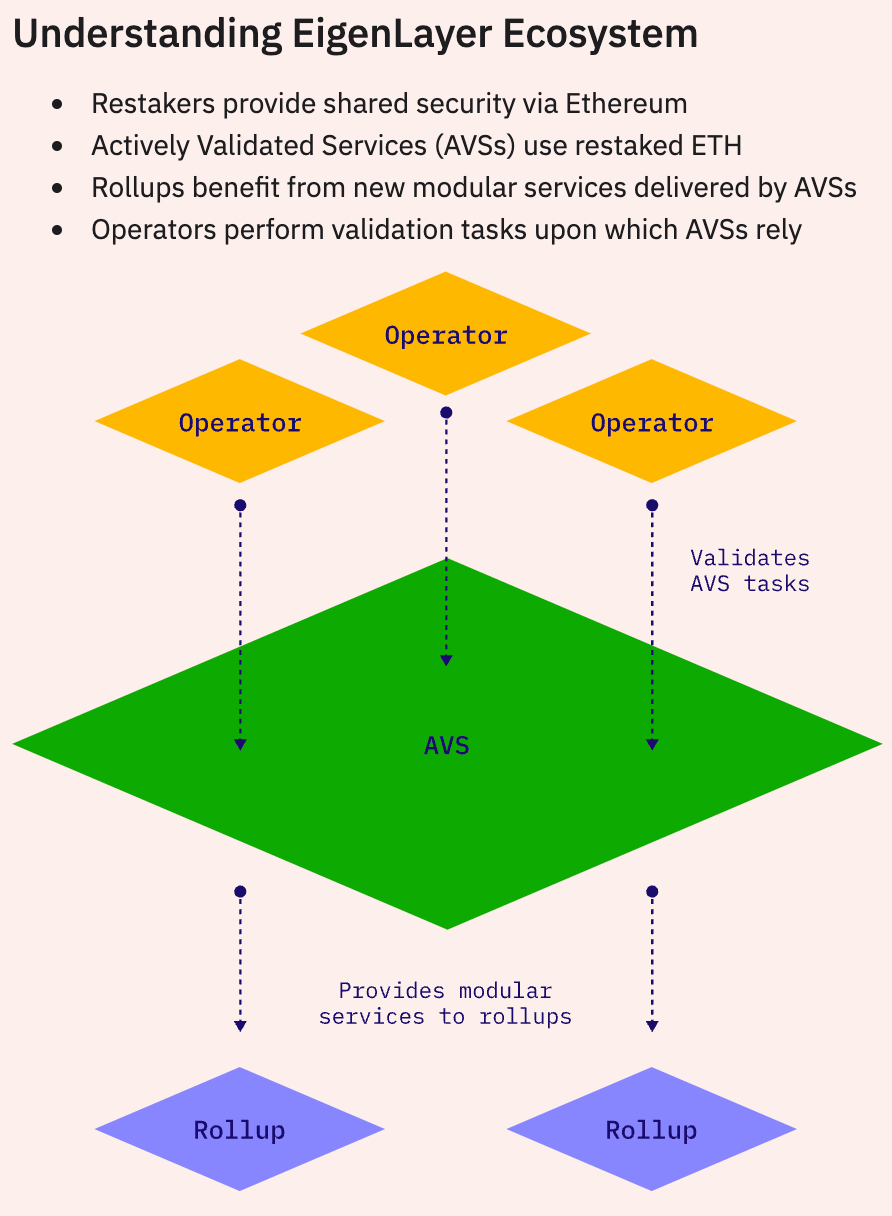

EigenLayer opened up a whole new playbook by allowing Ethereum validators to “opt in” to secure other protocols using their ETH that was already staked on the main chain. Because these validators had proven they could uphold network integrity for Ethereum, it made sense for smaller or newer projects to leverage that same pool of validators, as well as the proven security collateral behind them. It was a breakthrough that quickly gained traction—partly because it was a win-win proposition. Protocols gain robust security from day one, while stakers have the opportunity to earn additional rewards on top of their Ethereum staking yield.

EigenLayer collectively refers to these protocols as “modules” or “actively validated services (AVSs).” Each subsequent secured AVS specifies its own slashing conditions to encourage validators to act within the best interests of their network. Without these additional penalties, malicious validators could collectively target and attack vulnerable modules.

Restaking has a direct link to the phenomenon of liquid staking derivatives (LSDs). Many participants who stake ETH through LSD platforms can restake those derivative tokens into EigenLayer-supported projects without necessarily giving up the convenience and flexibility of holding a liquid asset. This synergy between LSDs and restaking is a major driver behind the market’s expanding size.

The Core Concept of Restaking

Although restaking borrows some concepts from liquid staking, it stands on its own as a distinct mechanism. With restaking, you take staked tokens—like ETH already locked for consensus—and use them as collateral or security for a secondary protocol. Essentially, you’re telling the new protocol, “I have these tokens staked, and if I behave maliciously here, you have the right to slash them.” Because the tokens remain staked on the original chain (like Ethereum), you’re effectively allowing more than one protocol to access that security deposit.

This multi-purpose security deposit benefits both sides. You, as the staker, can collect additional yield streams or tokens from the protocols you secure. Meanwhile, these protocols sidestep the usually daunting task of building a validator set from scratch. They can piggyback off Ethereum’s proven network of validators and the capital they have staked. Of course, it isn’t risk-free. If the protocol you’re securing fails or experiences malicious validator behavior, you could face slashing penalties. That risk, however, incentivizes participants to only restake on projects they trust.

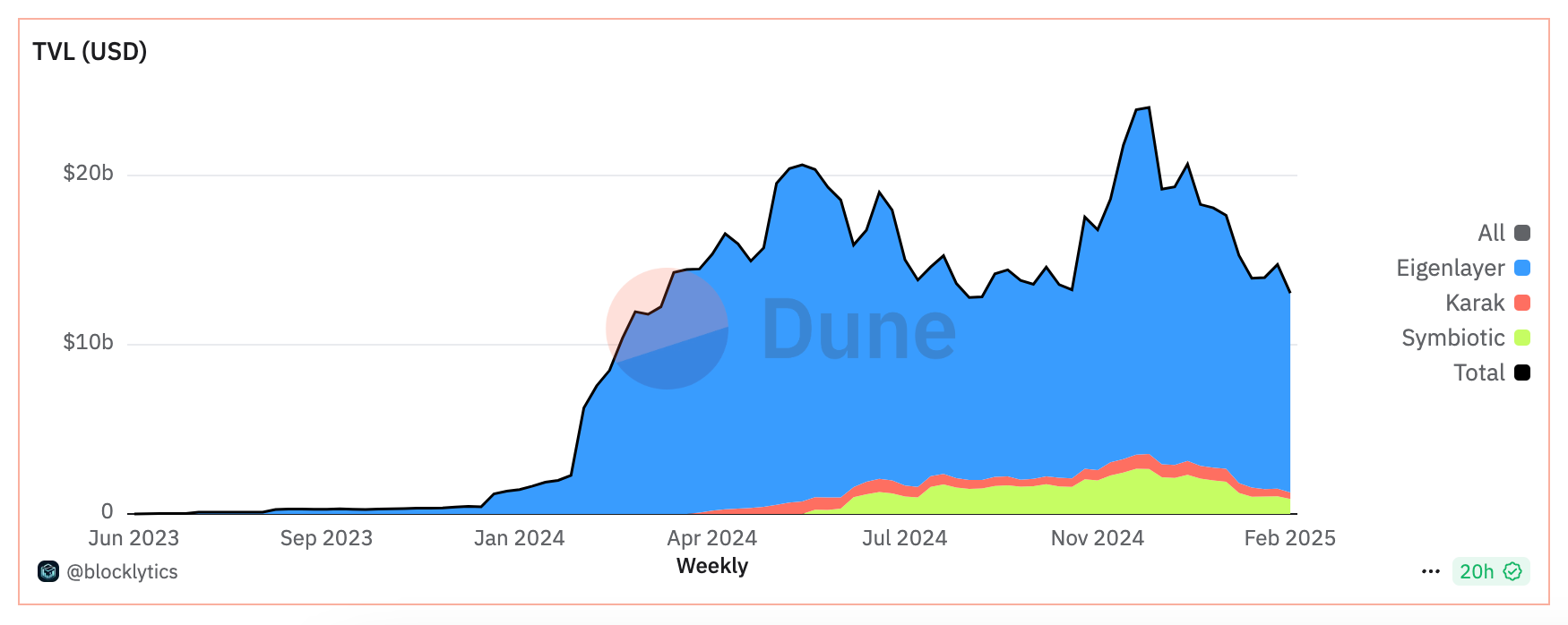

Over the past quarter, the total value locked in restaking protocols grew steadily—reaching north of $20 billion on the Ethereum ecosystem alone. The number of new restakers also doubled over that period, highlighting the broadening adoption among both institutional and retail participants. Much of the growth is attributed to users who already hold liquid staking derivatives and want to earn more yield without pulling out of their original staking positions.

Between February and April 2024, EigenLayer—widely regarded as the foremost restaking protocol—experienced a sizable influx of deposits, followed by consistent growth in total value locked (TVL). The platform’s TVL now exceeds 7.2 million ETH, translating and fluctuating to roughly $15-20 billion depending on ETH price. Of that figure, around 80.6% comprises native staked ETH, 14% is attributed to Lido’s stETH, and the remainder spans more than ten different liquid staking tokens (LSTs). The protocol currently has just shy of 137,000 unique depositors.

Restaking’s Expansion Beyond Ethereum

Though much of the initial excitement centers on Ethereum, the concept of restaking isn’t limited to that ecosystem. Other chains such as Solana (through Renzo, Jito, Solayer amongst others) have begun experimenting with variations of “shared security,” allowing tokens staked on their networks to be deployed for extra layers of protection within side-chains or partner protocols. For instance, certain networks using a “hub-and-zone” or “shared security” architecture already rely on a central set of validators to protect multiple sub-chains. These architectures are a natural breeding ground for restaking, because they allow capital to move more freely across different parts of the ecosystem.

Early data from these multi-chain expansions show that they’re attracting both new stakers and established validators looking to diversify their yield streams. When combined with LSDs, restakers can effectively participate in multiple ecosystems simultaneously—a powerful proposition for those with a more adventurous DeFi strategy.

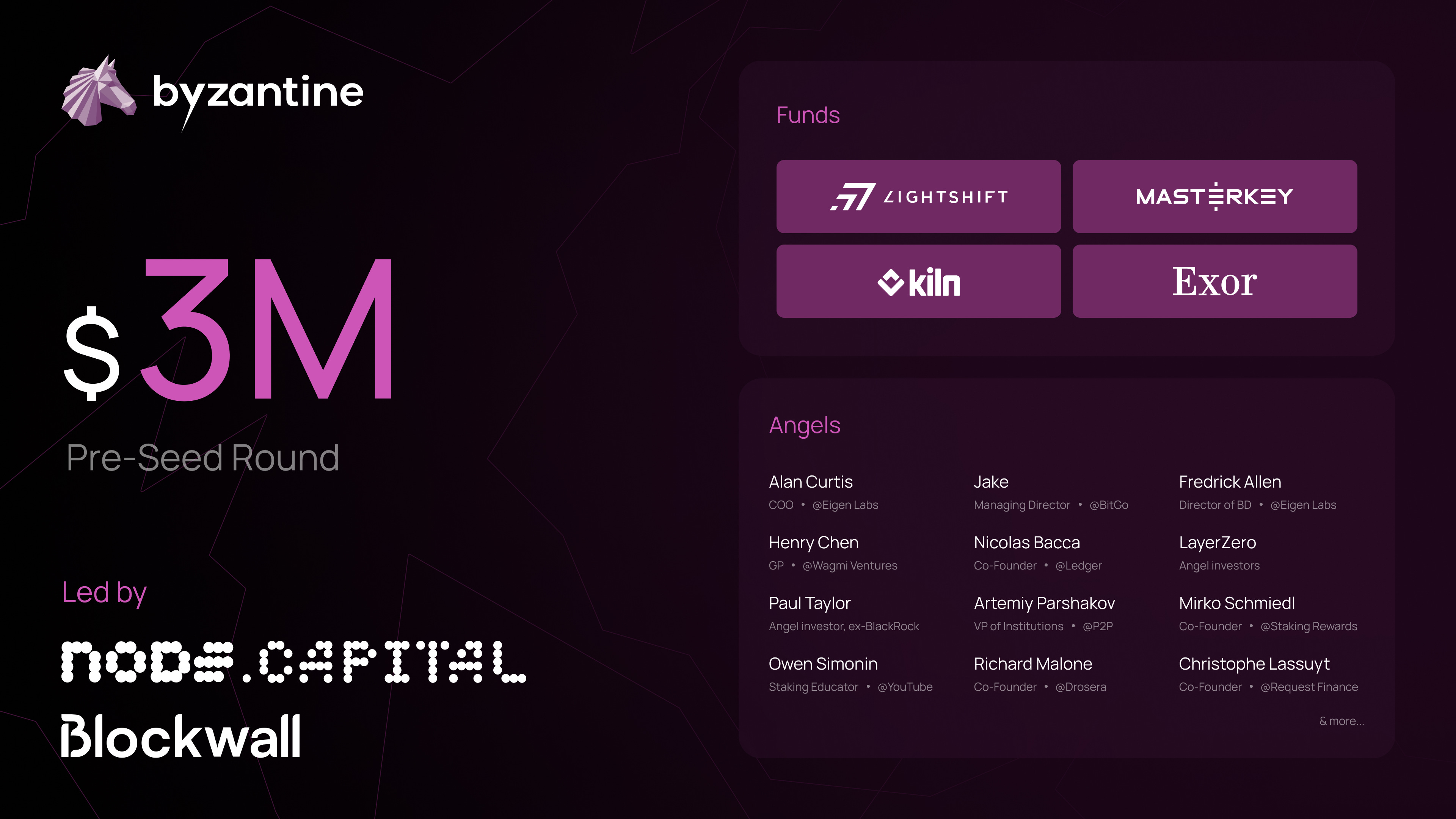

Introducing Byzantine.fi and why we invested

Amid all this excitement, we’re thrilled to announce our investment in Byzantine.fi—a project that embodies the potential we see in restaking. Byzantine aims to simplify the restaking process by consolidating opportunities across various chains into a single user-friendly interface. As such they are building a decentralized protocol making restaking accessible to all.

Designed to make restaking strategies permissionless and flexible, Byzantine supports more competitive, risk-optimized yield. As the first restaking aggregation layer, it empowers onchain users, including institutions, to do more with their assets. By acting as a hub for restaking, Byzantine seeks to make it easier than ever to discover, compare, and participate in restaking strategies. That means users can find yield opportunities on new protocols without having to juggle multiple dashboards or bridging solutions that—frankly speaking—is not really appealing to mainstream users.

We’re therefore thrilled to announce our commitment as a co-lead investor of Byzantine’s $ 3 million pre-seed round with our friends at Node Capital — supporting Gaia and Jonas 👋 in this great journey.

Platforms like EigenLayer paved the way by reusing Ethereum’s validator set, and the market has responded by pouring in billions in staked collateral. As other chains adopt similar models, cross-chain solutions gain traction, and LSDs continue to rise, we at Blockwall expect the restaking sector to keep growing. Our investment in Byzantine underscores our conviction that restaking represents a lasting shift in blockchain security—one that makes decentralized networks safer, more scalable, and more user-friendly all at once.

We’ll be watching this space closely (and participating in it), and we look forward to the new protocols that leverage restaking in creative ways. If the early numbers are any indication, we’ve only begun to scratch the surface of what restaking can do.

Disclaimer

To avoid any misinterpretation, nothing in this blog should be considered as an offer to sell or a solicitation of interest to purchase any securities advised by Blockwall, its affiliates or its representatives. Under no circumstances should anything herein be interpreted as fund marketing materials for prospective investors considering an investment in any Blockwall fund. None of the data and information constitutes general or personalized investment advice and only represents the personal opinion of the author. The author and/or Blockwall may directly or indirectly be exposed to the mentioned assets/investments. For further information please view the full Disclaimer by clicking the button below.

This work is licensed under the Creative Commons Attribution – No Derivatives 4.0 International License. CC BY-ND 4.0 Legal Code | Creative Commons